Heart disease is often discussed in terms of symptoms, treatment, and prevention.

What receives far less attention is what happens after a diagnosis is made.

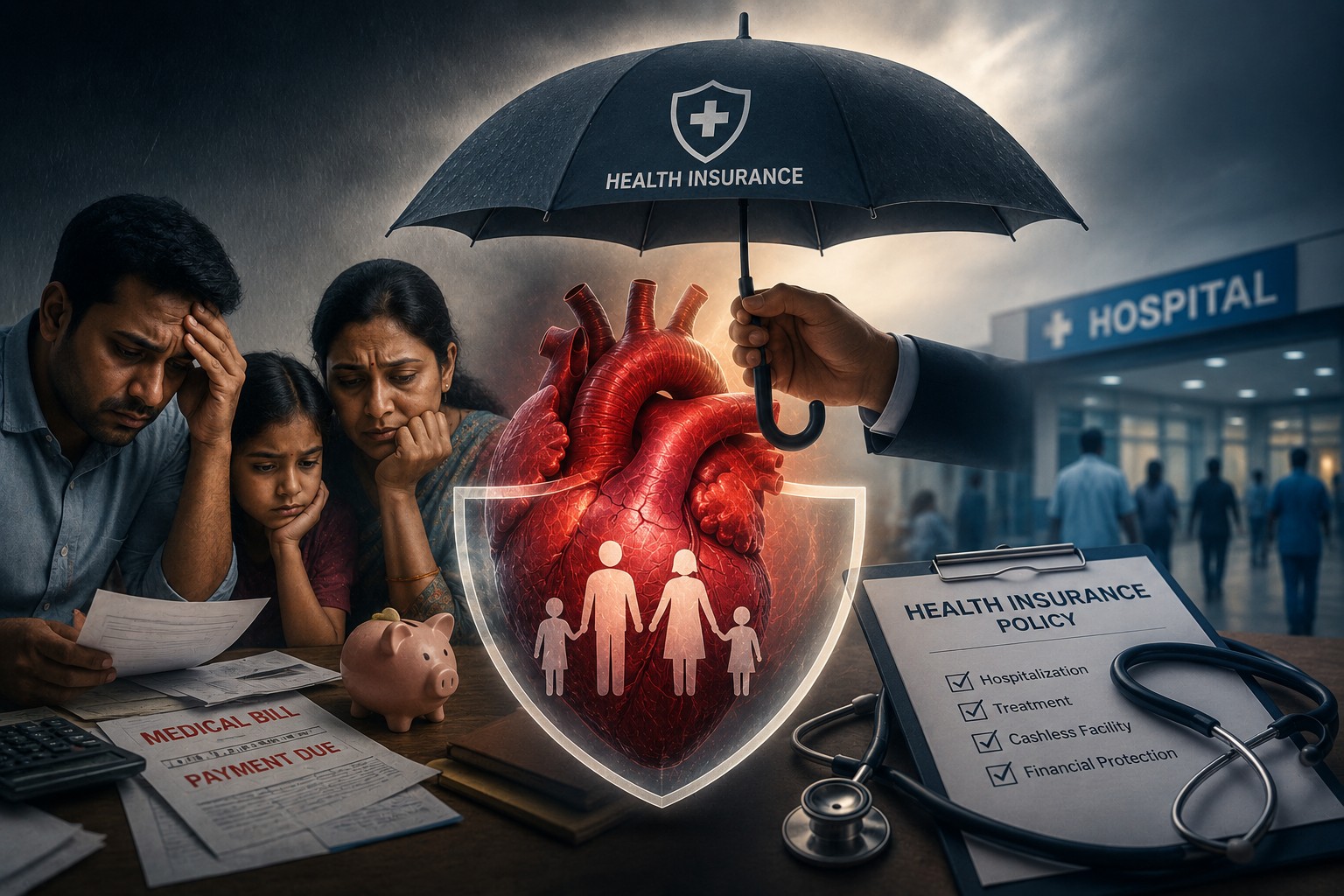

A heart attack, angioplasty, bypass surgery, or prolonged hospitalization can create not only a medical crisis but also a financial one.

For many Indian families, the first serious conversation about health insurance begins only after a cardiac emergency occurs.

Unfortunately, by then, some of the most important decisions can no longer be changed.

Waiting periods may apply. Coverage limits may be insufficient. Certain conditions may not be covered. Claims may take time. Documentation may be incomplete.

The result is additional stress at a time when families should be focusing on recovery.

Understanding how health insurance works before a medical emergency occurs can help families make better financial and healthcare decisions.

Why Heart Disease Creates Significant Financial Pressure

Heart conditions often require more than a single consultation.

Treatment may involve:

- Emergency hospitalization

- Diagnostic testing

- Angiography

- Angioplasty and stent placement

- Bypass surgery

- Intensive care

- Follow-up consultations

- Long-term medication

Depending on the hospital, city, and complexity of treatment, costs can range from tens of thousands to several lakhs of rupees.

Even families with stable incomes can find themselves under financial pressure when treatment costs arrive unexpectedly.

The Most Common Insurance Mistake: Buying Too Late

One of the biggest misconceptions about health insurance is that it can be purchased when a health issue appears.

In reality, many policies contain waiting periods before certain benefits become available.

If someone purchases insurance after being diagnosed with a significant heart condition, coverage options may become more limited.

This is why insurance is often most valuable when arranged before major medical issues arise.

Health insurance works best as preparation, not reaction.

Understanding Waiting Periods

Many people discover waiting periods only when they attempt to make a claim.

A waiting period refers to a specific duration during which certain conditions may not be covered.

Different policies have different rules, but waiting periods often apply to:

- Pre-existing conditions

- Specific procedures

- Certain chronic illnesses

This means that reading policy details carefully is important before purchase.

The cheapest premium is not always the most useful coverage.

Pre-Existing Conditions Matter

Heart disease is one of the areas where pre-existing condition clauses become particularly important.

A pre-existing condition may include:

- Hypertension

- Diabetes

- Existing heart disease

- Previous cardiac procedures

Families should always disclose medical history accurately during policy applications.

Failure to do so can create complications during claim processing later.

Transparency is essential.

Coverage Amount Matters More Than Many People Think

A common mistake is choosing a policy solely based on affordability.

While affordability matters, insufficient coverage can create challenges during major medical events.

For example, a policy with a low coverage limit may not fully cover:

- Angioplasty

- Cardiac surgery

- ICU care

- Extended hospitalization

As medical costs continue to rise, coverage adequacy deserves careful consideration.

Cashless vs Reimbursement: Know the Difference

Many policyholders are unfamiliar with how claims are processed.

Cashless Treatment

In a cashless arrangement, the insurer directly settles approved expenses with a network hospital.

This reduces the immediate financial burden on families.

Reimbursement Claims

Under reimbursement, families initially pay expenses and later submit documentation to seek repayment.

Understanding how a policy operates can help avoid surprises during emergencies.

Documentation Can Become a Challenge

During medical emergencies, paperwork is rarely anyone’s priority.

Yet documentation remains essential.

Important records often include:

- Hospital bills

- Diagnostic reports

- Prescriptions

- Discharge summaries

- Identity documents

- Insurance cards

Keeping records organized before an emergency occurs can make the claims process significantly smoother.

Insurance Does Not Replace Prevention

One misunderstanding worth addressing is that insurance and prevention serve the same purpose.

They do not.

Insurance helps manage financial risk.

Prevention helps reduce health risk.

A policy cannot eliminate:

- High blood pressure

- Diabetes

- Poor lifestyle habits

- Delayed diagnosis

Regular health screenings and healthy habits remain important regardless of insurance status.

Why Younger Adults Should Care Too

Many people associate health insurance with retirement planning.

However, heart disease is increasingly affecting younger adults in India.

Factors contributing to this trend include:

- Sedentary lifestyles

- Stress

- Diabetes

- Obesity

- High cholesterol

Waiting until later in life to think about insurance can reduce available options and increase costs.

Earlier planning often provides greater flexibility.

Questions Families Should Ask Before Buying a Policy

Before selecting a health insurance plan, consider asking:

- What is the waiting period for pre-existing conditions?

- What is the total coverage amount?

- Are major cardiac procedures covered?

- Which hospitals are included in the network?

- Are there sub-limits for specific treatments?

- What is the claims process?

Understanding these details can help families make more informed decisions.

The Bigger Lesson: Financial Preparedness Is Part of Health Preparedness

Heart disease affects more than the body.

It affects families, routines, finances, and long-term planning.

Medical preparedness and financial preparedness often go hand in hand.

A well-informed family is better positioned to focus on treatment and recovery rather than navigating financial uncertainty during a crisis.

Final Thoughts

Health insurance may not prevent heart disease, but it can help reduce financial uncertainty when treatment becomes necessary.

The best time to understand a policy is before it is needed, not during a medical emergency.

By learning about coverage, waiting periods, exclusions, and claim processes early, families can make decisions with greater confidence and clarity.

Because when a heart-related emergency occurs, the focus should be on care and recovery—not financial confusion.